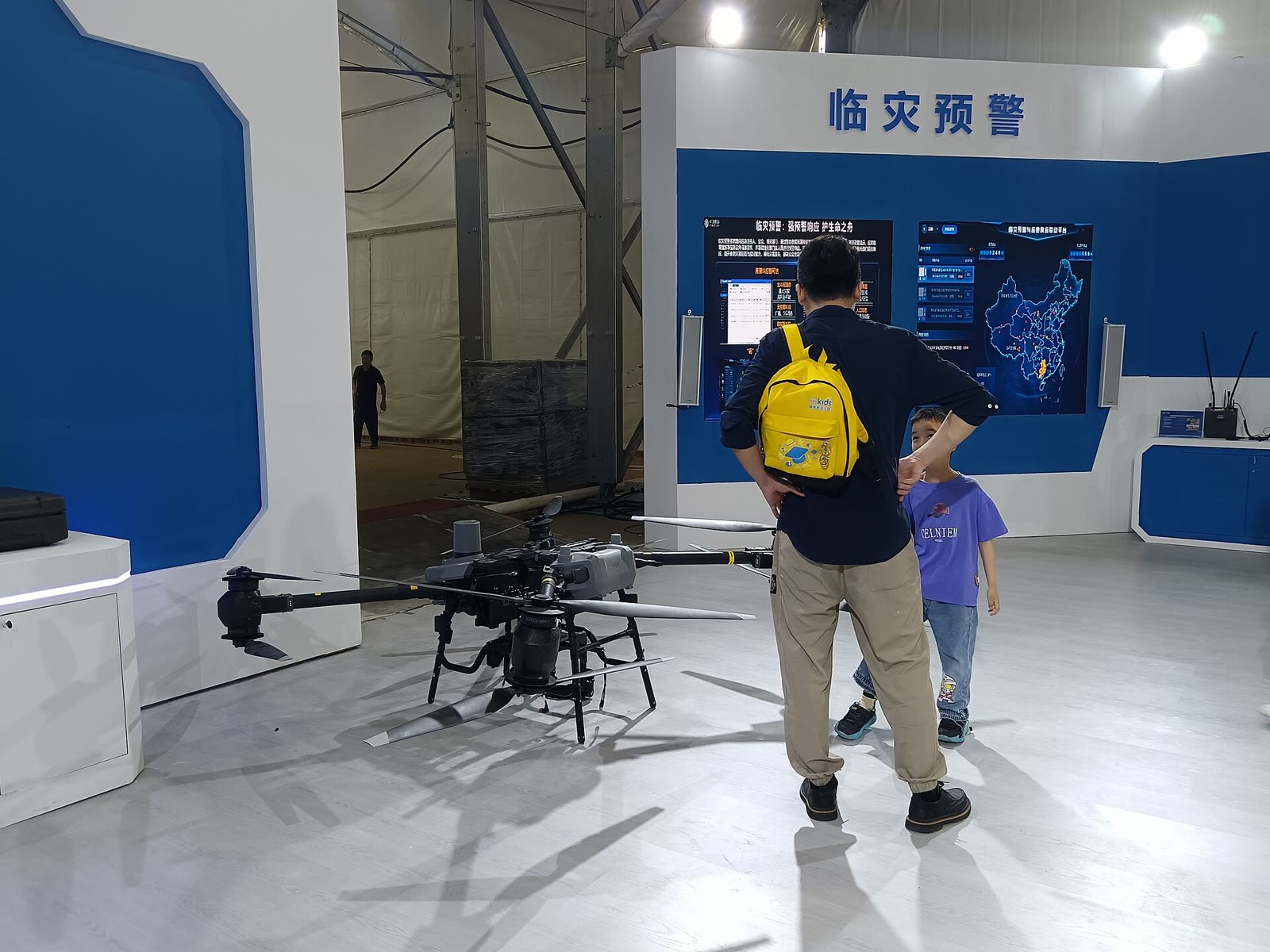

The most revealing object in China Mobile's exhibition booth is not a chatbot screen. It is a large drone parked beneath a wall marked disaster warning, while a visitor and child study the machinery. The photograph does not tell us whether a foundation model controls anything in the display. That uncertainty is useful. It directs attention away from the model name and toward the system a telecom operator can assemble around it: a connected device, a live data path, remote compute, an application, and people who can install and support the whole package.[5]

That is the underappreciated signal in the 2025 reports from China Mobile, China Telecom, and China Unicom. All three still promote their own model or platform brands—Jiutian, Xingchen, and Yuanjing/UniAI—but their disclosures increasingly describe AI as a stack that begins below the model and ends well beyond it. Compute clusters, optical networks, cloud control planes, data engineering, agents, consumer accounts, enterprise contracts, and local delivery teams now sit in the same operating story.[1][2][3]

As of July 17, 2026, China's carrier AI race is therefore better read as a contest over distribution than as a three-way model leaderboard. The carriers do not need to own the best model for every task. Their stronger position is the ability to place a chosen model—proprietary, open, or third-party—inside infrastructure and customer relationships that already reach homes, factories, government offices, vehicles, and field equipment.

The model is becoming one layer in a carrier stack

China Mobile's 2025 report shows the clearest move from research brand to product organization. The company launched Jiutian 3.0, more than 100 AI products and application solutions, 29 industry agents, and more than 50 proprietary industry models. It also established a dedicated Jiutian AI company and research institute. Beneath that product layer, China Mobile reported 92.5 EFLOPS of total intelligent-computing capacity and a three-tier network designed around latency within cities, provinces, and the country.[1]

The commercial surface is already large, although its boundary is broad. China Mobile reported RMB90.8 billion in AI-services revenue for 2025, up 5.3% year on year, while its Lingxi assistant reached 117 million monthly active customers. Its report defines AI services as a major business category alongside communications and computing, not as foundation-model API revenue alone. Those figures demonstrate distribution; they do not reveal how much money came from tokens, software licenses, integration, data services, media products, or established digital services with AI features.[1]

China Telecom describes a more explicitly layered architecture. Its Xirang-centered intelligent cloud runs from infrastructure and data through the Xingchen model family to applications. The company reported 91 EFLOPS of self-owned and accessed intelligent compute, a corpus above 10 trillion tokens, more than 500 TB of higher-quality datasets across 14 industries, over 110 industry models, and more than 350 industry agents serving over 37,000 customers. It also said intelligent revenue reached RMB12.3 billion, a category that combines AI and intelligent-computing services.[2]

The revealing phrase in China Telecom's 2026 outlook is its intention to make token services a main line of business. That frames the carrier less as a lab selling one model and more as a utility attempting to meter an entire production path: compute, storage, network, routing, model access, security, and application delivery. Whether that path produces attractive utilization and margins is still an open question, but the operating ambition is unusually concrete.[2]

China Unicom's disclosure points to a more open aggregation strategy. It reported 45 EFLOPS of intelligent compute and positioned Unicom Cloud around a bundle of applications, models, and resources. Its UniAI platforms offered more than 140 mainstream models, held over 400 TB of higher-quality datasets, and gathered more than 10,000 developers. The same report says Unicom Cloud supported more than 180 province- and city-level government-cloud projects and digital work for nearly 400,000 corporate customers.[3]

This is not simply a smaller version of the other two stacks. A platform offering many mainstream models can compete through orchestration and delivery even when another lab releases the strongest checkpoint. Unicom also reported that AI revenue grew by more than 140% in 2025, but did not publish the absolute amount in the cited overview; its definition includes intelligent compute, models and agents, data services, and related work. The growth rate is a field signal, not a basis for ranking revenue against the other carriers.[3]

The installed base is the strategic asset

The Ministry of Industry and Information Technology's 2025 industry bulletin supplies the scale underneath those company reports. By year-end, China had 1.204 billion 5G mobile users, 2.888 billion mobile-IoT terminal connections, 4.838 million 5G base stations, and 938,000 data-center racks offered externally by the three basic telecom enterprises. Revenue from emerging services such as cloud, big data, mobile IoT, and data centers reached RMB450.8 billion, or 25.7% of telecom-industry revenue.[4]

None of those numbers measures AI use. A 5G account does not become an agent user, an IoT connection does not imply model inference, and a rack says nothing about utilization. Together, however, they map the carriers' distribution surface. A specialist model company may supply a better model. A carrier can potentially supply the identity, connection, edge gateway, cloud region, bill, service desk, and enterprise account surrounding it.

That changes what “last mile” means. It is not only the cable or radio link between a network and a user. For enterprise AI, the last mile also includes procurement, data access, deployment inside an approved environment, integration with an existing workflow, and someone accountable when the system fails. China's carriers already maintain local organizations built for those tasks. Their AI opportunity is to make that old distribution machinery carry a new class of service.

The Changsha drone makes the point without proving too much. A disaster-warning system may require sensing, positioning, image or video analysis, low-latency communication, a command platform, human escalation, and maintenance in the field. The photograph verifies only that China Mobile exhibited the aircraft in that setting.[5] It does not verify the software architecture. But it illustrates why a carrier's defensible product is likely to be the joined-up service, not an isolated model endpoint.

Three numbers that should not become a leaderboard

The reports invite comparison, but not simple addition. China Mobile's 92.5 EFLOPS includes self-built and rented capacity. China Telecom gives 91 EFLOPS for self-owned and accessed capacity, then separately identifies 46 EFLOPS as self-owned. China Unicom reports 45 EFLOPS. Because leased or accessed resources can overlap with another provider's infrastructure, and because hardware mix and utilization are not disclosed on a common basis, the three headline figures are neither additive nor a clean performance ranking.[1][2][3]

The revenue labels are even less comparable. China Mobile's AI-services category is much larger and sits inside its own business taxonomy. China Telecom's “intelligent revenue” combines AI and intelligent compute. China Unicom reports a growth rate for a category spanning compute, models, agents, and data but no absolute amount in its overview. These are useful signs that AI has entered budgeting and reporting. They are not standardized market-share data.[1][2][3]

Product counts have the same boundary. One hundred products, 350 agents, or 140 available models describe supply. They do not disclose how many customers use each product repeatedly, how often an agent completes a task, what share of inference is served by the carrier's own models, or whether the deployment improves an outcome. Catalog breadth can be valuable, especially for distribution. It is not adoption by itself.

The same caution applies to consumer reach. China Mobile's 117 million monthly active Lingxi customers and China Unicom's more than 300 million cloud-AI product users show access to enormous account bases. The labels cover different products and engagement definitions, so they should not be placed in one ranking. The proof of an AI distribution advantage will be sustained use of specific capabilities, not the number of legacy accounts to which an AI feature can be offered.[1][3]

What would turn distribution into an advantage

First, watch for comparable workload disclosure. Tokens processed, accelerator utilization, latency by service class, recurring revenue, and the split between compute, software, and integration would say more than aggregate EFLOPS or an expanding agent catalog. China Telecom's decision to foreground token services makes this especially worth tracking.[2]

Second, watch model neutrality. A carrier platform becomes more useful if customers can move among Jiutian, Xingchen, Yuanjing, open models, and third-party systems without rebuilding identity, monitoring, data controls, and billing. The reports already acknowledge multi-model environments, but portability should be tested through actual interfaces, migration costs, and service-level terms rather than platform counts.[1][2][3]

Third, watch field outcomes. For a factory, hospital, government office, or disaster-response unit, a deployment should be judged by a disclosed baseline: less downtime, faster handling, fewer missed events, lower energy use, or another task-specific result. Carrier case counts and customer totals establish reach. Independent or customer-published outcome measures would establish value.

Finally, watch where accountability lands. A carrier that bundles the network, compute, model, and application has fewer places to point when the service fails. That concentration can be a selling point—one contract and one support path—but only if incident reporting, model-version records, data governance, and human escalation travel with the bundle.

China's carriers are unlikely to win every model comparison, and they do not need to. Their more durable contest is to make AI arrive as a working service at the edge of a network and the center of a customer's workflow. The drone on the exhibition floor is a better emblem for that race than another benchmark slide: the intelligence matters, but so do the radio link, cloud, operator, maintenance crew, and person who must act on the warning.

Sources

- China Mobile Limited, Annual Report 2025 (published April 2026)—Jiutian 3.0, AI products and agents, computing capacity, Lingxi usage, AI-services revenue, and the creation of the Jiutian AI organization.

- China Telecom Corporation Limited, Annual Report 2025 (published April 2026)—Xirang and Xingchen architecture, compute and data disclosures, industry-model and agent counts, intelligent revenue, and the token-services outlook.

- China Unicom (Hong Kong) Limited, Annual Report 2025 (published April 2026)—UniAI platforms, Yuanjing RAG, compute capacity, model and developer counts, customer distribution, cloud-AI products, and the company's AI-revenue definition.

- Ministry of Industry and Information Technology of China, “2025 Statistical Bulletin of the Communications Industry” (2026)—official preliminary statistics for telecom revenue, 5G users and base stations, mobile-IoT connections, and external data-center racks.

- Huangdan2060, “Unmanned aerial vehicle of China Mobile, 2025 Changsha International Construction Equipment Exhibition (A)” (photographed May 17, 2025)—source page and metadata for the documentary article image.