As of 2026-03-09 23:31 UTC, the U.S. power narrative is often told as a generation race: more gas, more renewables, more data-center load, and more interconnection requests. The more operational bottleneck has moved one layer deeper into hardware logistics: getting enough transformers, in the right specifications, on the right timetable.

This is no longer a niche procurement complaint. Across federal analysis, industry reporting, and utility-facing guidance, the same signal repeats: lead times have stretched from months to multi-year windows, and those delays are now influencing reliability planning, customer connections, and capex sequencing.[2][4][5][6]

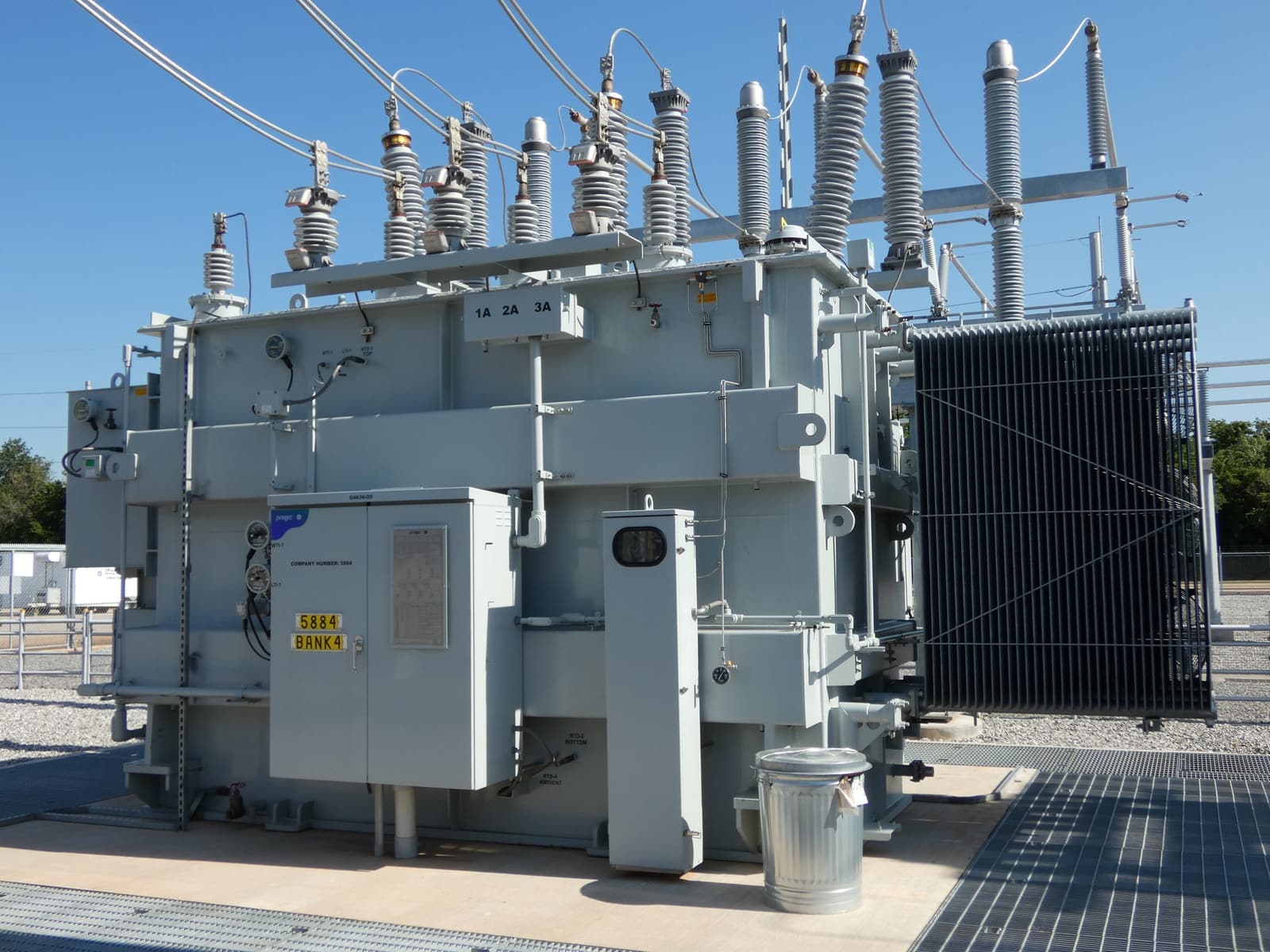

Image context: The hero image shows a high-voltage substation transformer yard, included to ground the piece in the exact equipment layer now driving delivery risk rather than generic grid visuals.

What the evidence says has changed

Three numbers define the shift:

- DOE reports distribution-transformer order windows moved from roughly 3–6 months (2019) to 12–30 months (2023), with utility trade members describing average lead-time escalation of 443% between 2020 and 2022.[2]

- The NIAC report submitted through CISA cites market evidence of transformer lead times rising from around 50 weeks (2021) to roughly 120 weeks (2024 average), with large transformer categories ranging about 80–210 weeks.[4]

- Reuters Events reporting (citing Wood Mackenzie) put U.S. second-quarter 2025 average delivery at about 143 weeks for GSUs and 128 weeks for power transformers.[5]

At the same time, demand pressure has not eased. EIA now projects U.S. electricity use to rise 1% in 2026 and 3% in 2027, describing the strongest four-year demand growth stretch since 2000 and explicitly tying that rise to large computing facilities.[1]

In short: demand is accelerating while critical hardware remains on extended clocks.

Why this bottleneck is harder than “build more factories”

The investigation points to a stacked constraint, not a single root cause.

First, specification fragmentation is slowing production throughput. DOE notes the industry has carried an extremely wide set of utility-specific distribution-transformer configurations (described as more than 80,000 varieties), which limits interchangeability and batch-scale manufacturing efficiency.[2]

Second, material and labor dependencies remain exposed. DOE and NIAC both describe pressure around grain-oriented electrical steel, copper/aluminum inputs, skilled labor pipelines, and manufacturing capacity expansion timelines.[2][4]

Third, capital and logistics frictions reduce reserve buffers. GAO documents utility testimony that large power transformers can cost up to about $10 million each, with transport costs reaching hundreds of thousands of dollars, making spare inventory hard for smaller entities to maintain.[3]

This is why the current constraint behaves differently from a normal procurement delay. A late transformer can defer energization even when land, permits, and generation-side capex are already committed.

Counterweight: supply response is real, but timing is the issue

There is meaningful evidence that the supply side is reacting:

- DOE has launched transformer-focused support and R&D pathways, including an $18 million Flexible Innovative Transformer Technologies (FITT) funding program and additional programs linked to manufacturing and resilience.[6]

- Large manufacturers have announced U.S. capacity expansion plans; Reuters Events summarizes a multi-company investment wave and Wood Mackenzie expectations that deficits could narrow by decade-end if projects execute as planned.[5]

So this is not a “no response” story. It is a timing mismatch story: demand growth is arriving now, while manufacturing normalization is still staged over multiple years.

What this means for operators and policymakers in 2026

The practical risk is no longer just underbuilding generation. It is mis-sequencing the grid stack:

- Announce load or generation additions.

- Assume hardware follows on historical timelines.

- Discover transformer delivery dates force reordering of construction and commissioning.

That sequence creates three second-order effects:

- Reliability exposure when replacement cycles collide with storm recovery and growth projects.

- Cost creep as long lead windows and expedited logistics raise project carrying costs.

- Queue distortion when project timelines are revised repeatedly around equipment certainty rather than engineering readiness.

Falsifier and watchlist

This investigation weakens if delivery windows normalize quickly and broadly. A credible falsifier would be sustained evidence over the next 12–18 months that:

- average lead times for key transformer classes fall back toward pre-2020 ranges,

- standardization efforts materially reduce custom-spec cycle times,

- and utility reserve coverage improves without acute cost escalation.

What to watch now:

- Updated average lead-time disclosures (GSU/power/distribution classes) from major market trackers and utility filings.[4][5]

- Evidence that DOE-industry standardization work is translating into repeatable catalog configurations and shorter procurement cycles.[2][6]

- Whether demand growth projections (especially data-center-linked) continue to rise faster than component delivery recovery.[1]

- Progress on reserve and mutual-support frameworks for utilities that cannot finance large standalone spares.[3]

The key policy implication is straightforward: in this phase of U.S. grid expansion, transformer delivery should be treated as a planning variable at the same level as permitting, fuel assumptions, and financing—not as a late-stage purchasing detail.

Sources

- U.S. EIA (2026-01-13), EIA forecasts strongest four-year growth in U.S. electricity demand since 2000, fueled by data centers

- U.S. DOE Office of Electricity (2024-02-22), DOE and Industry Team Up to Keep the Lights On for America

- U.S. GAO, Electricity Grid: DOE Could Better Support Industry Efforts to Ensure Adequate Transformer Reserves (GAO-23-106180)

- National Infrastructure Advisory Council via CISA (2024), Addressing the Critical Shortage of Power Transformers to Ensure Reliability of the U.S. Grid (PDF)

- Reuters Events (2025-12-01), Grid equipment makers invest in US to ease supply shortage

- U.S. DOE Office of Electricity, R&D Efforts to Address Transformer Supply

- Wood Mackenzie press release, Power transformers and distribution transformers will face supply deficits of 30% and 10% in 2025

- Wikimedia Commons image source, Substation Power Transformer 1.jpg