Most hyperinflation stories are told as morality plays about fiscal irresponsibility, but that framing misses the operational question that mattered in both Weimar Germany (1923) and Brazil (1994): how do you get people to quote tomorrow’s prices in something they believe, before they trust the official money again?

This comparison treats stabilization as a sequencing problem rather than a slogan. In both cases, authorities eventually assembled a two-step mechanism: first, create a credible bridge unit for contracts and price memory; second, impose monetary-fiscal constraints that prevent immediate relapse. The details differed sharply, yet the structural logic rhymed.

Timeline anchors: where each break actually started

- Germany, 15 Nov 1923: Rentenmark introduced after the Papiermark collapse; conversion set at 1 Rentenmark = 1 trillion (10^12) old marks and near prewar parity at US$1 = 4.2 RM.[2]

- Germany, late 1923: during peak breakdown, the dollar value of the mark reached roughly 4.2105 trillion marks per US$1 in November 1923.[1]

- Brazil, Mar 1994: URV (Unidade Real de Valor) launched as a non-cash reference unit to separate price-setting from cruzeiro-real inflation inertia.[3][4]

- Brazil, 1 Jul 1994: URV converted at parity into the new legal currency (1 real = 1 URV = CR$2,750).[3][4]

- Brazil, 1995–1998: annual CPI inflation fell from four digits to double digits and then single digits in the World Bank series (1994: 2075.9%, 1995: 66.0%, 1996: 15.8%, 1997: 6.9%, 1998: 3.2%).[5]

What failed before success: money issuance without a pricing anchor

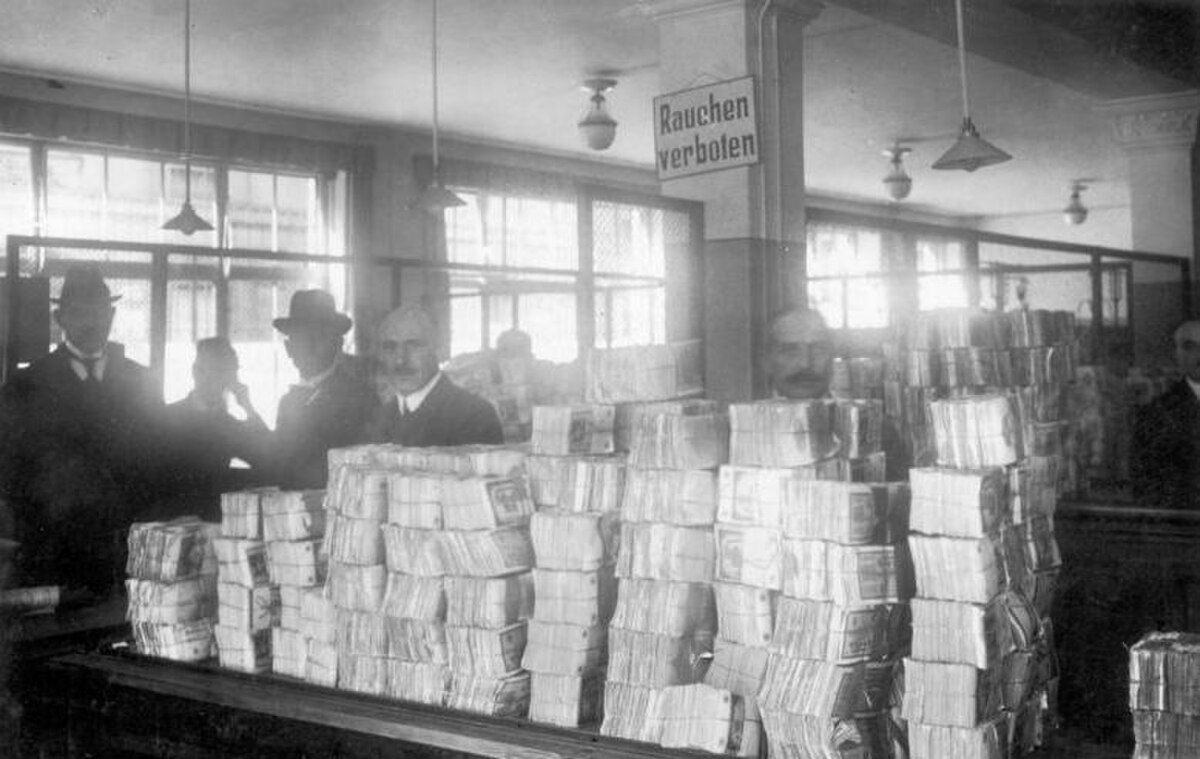

In Germany, wartime financing and postwar disorder were followed by a policy regime that could not stop nominal acceleration once confidence collapsed. The exchange-rate spiral and domestic price spiral reinforced each other, and by 1923 money ceased to perform its store-of-value and unit-of-account roles in daily life.[1]

Brazil’s pre-1994 sequence had a different institutional surface but a comparable behavioral trap: formal stabilization attempts repeatedly failed because indexation and expectation-reset routines kept reproducing inflation even when specific nominal controls were announced. The system could absorb temporary shocks but not break inertial repricing habits.[3][4]

In both cases, the missing component was not simply austerity rhetoric. The missing component was a working denominator for contracts.

The core comparative mechanism: bridge unit first, full trust later

Germany’s Rentenmark and Brazil’s URV were not identical instruments, but both functioned as bridge architectures.

Germany 1923: asset-backed bridge plus issuance stop

The Rentenmark was introduced through a conversion shock that created a clean nominal reset. The old money remained in memory, but the new unit offered a focal rate that households and firms could coordinate around. Critically, stabilization was reinforced by stopping the previous uncontrolled expansion path and tightening the policy regime around the new unit.[1][2]

The key move was therefore institutional, not merely symbolic: the new denominator and issuance discipline arrived together, reducing the probability that today’s quoted price would be invalid by tomorrow.

Brazil 1994: non-cash unit of account before legal tender swap

Brazil’s URV mechanism explicitly targeted inertial inflation. Prices were quoted in a stable reference unit while payments still occurred in the old currency, allowing a gradual migration of expectations. When the real replaced the cruzeiro real in July 1994, large parts of the economy had already adapted price memory to the new reference frame.[3][4]

This was a subtler bridge than Weimar’s conversion shock: instead of immediate replacement as the only first step, Brazil used a transitional accounting layer that taught agents to think in a stable unit before legal conversion day.

Numeric anchors that expose the difference in speed and depth

- Weimar endpoint signal: ~4.2105 trillion marks per US$1 at peak collapse in Nov 1923.[1]

- Weimar conversion scale: 1 RM = 10^12 old marks.[2]

- Brazil pre-break level: annual CPI inflation above 1,900% in 1993 and above 2,000% in 1994 in the World Bank annual series.[5]

- Brazil post-break trajectory: to 66.0% (1995), 15.8% (1996), 6.9% (1997), 3.2% (1998).[5]

The analytical value of this comparison is that both episodes show a credibility transition, but the tempo differed: Germany’s move looked like abrupt nominal rupture; Brazil’s looked like staged unit migration followed by legal replacement.

What this comparison can and cannot claim

It is tempting to reduce both cases to “just fix fiscal policy,” but that flattens the historical mechanism. Fiscal and monetary tightening were necessary in both, yet each case also required a practical coordination device for everyday pricing behavior.

The stronger comparative claim is narrower:

- Hyperinflation ends durably only when policy can re-anchor the unit of account people use in contracts.

- The re-anchoring usually needs a bridge form (hard conversion or transitional reference unit) before full credibility of legal tender is restored.

- Enforcement discipline must arrive fast enough that the bridge is not read as another temporary trick.

Why this still matters beyond textbook history

Modern high-inflation episodes often focus on reserves, deficits, and central-bank language. Those are necessary variables, but Weimar and Brazil suggest a practical implementation test that is frequently underweighted: can households and firms quote next month in a unit they expect to survive?

If the answer is no, policy has not yet crossed the stabilization threshold, even if headline announcements are dramatic.

Invalidation boundary

This comparative interpretation would weaken if stronger archival and statistical evidence showed that expectation re-anchoring in both cases happened before bridge-unit mechanisms were introduced, with bridge instruments only following as cosmetic codification. Current source synthesis supports the opposite ordering, but that ordering remains the decisive empirical hinge for this argument.[1][2][3][4][5]

Sources

- Wikipedia — Hyperinflation in the Weimar Republic

- Wikipedia — Rentenmark

- Wikipedia — Plano Real

- Wikipedia — Unidade real de valor (URV)

- World Bank API — Brazil CPI inflation, annual % (FP.CPI.TOTL.ZG)

- Encyclopaedia Britannica — Hyperinflation (concept context)